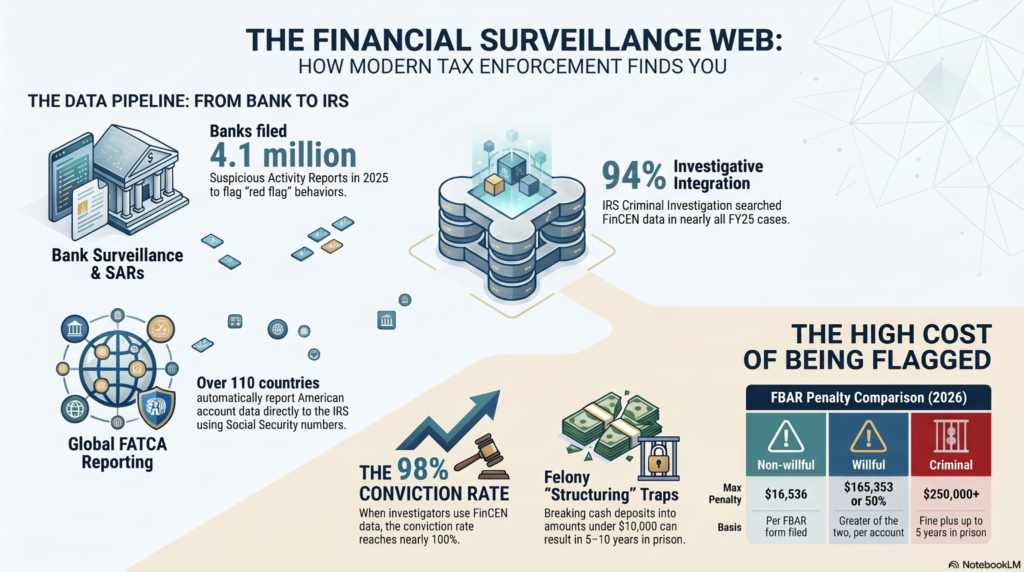

The IRS no longer waits for a tax return to flag a problem. FinCEN tax compliance data, bank reports, and cross-border filings now reach federal investigators before most taxpayers ever see an audit letter. In fiscal year 2025 alone, banks filed more than 2.19 million Suspicious Activity Reports, and the IRS Criminal Investigation searched that data in 94% of its cases.

A web of FinCEN regulations, FATCA agreements, and Bank Secrecy Act rules now connects your bank, your tax preparer, and the federal government in ways most people never see until a notice arrives.

This article breaks down how that surveillance network actually works, what triggers an audit, and what your options look like once you are flagged.

| Key TakeawaysBanks filed 4.1 million Suspicious Activity Reports in 2025, up nearly 8% from 2024IRS-CI identified $10.59 billion in financial crimes in FY25, a 15.7% jump from FY24Non-willful FBAR penalties can reach $16,536 per report in 2026; willful penalties can reach $165,353 or 50% of the account balanceDomestic U.S. companies are currently exempt from Corporate Transparency Act beneficial ownership reporting; only foreign-formed entities must still fileThe IRS closed public comment on a revised Voluntary Disclosure Practice on March 22, 2026 |

The Convergence of AML Tax Compliance and Federal Audits

Federal tax audits and anti-money laundering enforcement now run on the same data pipeline. A bank’s fraud desk and an IRS auditor often pull information from the identical financial crime enforcement network database, just for different reasons.

Decoding the Mandate of the Financial Crime Enforcement Network

The Financial Crime Enforcement Network, known as FinCEN, is a bureau of the U.S. Department of the Treasury that collects and analyzes financial transaction data to fight money laundering and tax evasion. It administers the Bank Secrecy Act, the law that requires banks and other institutions to report large or suspicious transactions.

FinCEN does not audit tax returns itself. Instead, it builds the data backbone that the IRS, the DOJ Tax Division, and other agencies query when they investigate a taxpayer.

Under current FinCEN regulations, more than a dozen categories of financial institutions, including banks, casinos, and money services businesses, must file reports whenever a transaction meets specific dollar thresholds or behavioral red flags.

How Suspicious Activity Reports (SARs) Feed Directly Into IRS Pipelines

A Suspicious Activity Report, or SAR, is a confidential filing a bank submits to FinCEN when it suspects a transaction involves fraud, money laundering, or an attempt to dodge a reporting rule. Banks filed 2.19 million SARs in 2025, and all seven categories of filers combined for 4.1 million reports, a record high.

IRS Criminal Investigation used Bank Secrecy Act data in 94% of its FY25 cases, running more than 3.9 million searches. Nearly 80% of those investigations involved a subject already named in a SAR. When agents use that data, the conviction rate hits 98%, with average prison terms of 42 months.

The Mechanics of Modern FinCEN Tax Compliance Tracking

FinCEN tax compliance tracking works through three connected layers: bank reporting, third-party data matching, and cross-border information exchange.

Automated FinCEN Data Sharing: The Death of Financial Privacy

Foreign banks now report American account holders to the IRS automatically through FATCA agreements signed with more than 110 countries. Since 2014, this has given the IRS near-complete visibility into offshore accounts held by U.S. citizens, even those who never set foot in the United States.

FATCA data sharing can trigger IRS audits within months of a foreign bank’s annual filing because the data arrives matched to a taxpayer’s Social Security number.

How Third-Party TIN and ITIN Onboarding Feeds the Surveillance Network

Every time a bank, brokerage, or payment processor opens an account, it collects a Taxpayer Identification Number or Individual Taxpayer Identification Number and verifies it against IRS records. This onboarding step, required under AML tax compliance rules, creates a permanent link between the account and the taxpayer’s federal filing history.

If the name, TIN, or address on file does not match IRS records, the institution must file a report. Multiplied across millions of accounts, this single verification step builds much of the data that investigators later use to identify unreported income or undisclosed entities.

Cross-Border Tracking Frameworks: Flagging Foreign Entity Structures

Beyond FATCA, the U.S. participates in information exchange frameworks similar to the global Common Reporting Standard, allowing tax authorities in different countries to swap account data. FBAR and FATCA reporting requirements for U.S. expats sit at the center of this system, since expats are statistically more likely to hold qualifying foreign accounts.

These frameworks specifically flag structures like shell companies, nominee directors, and layered ownership chains. A foreign entity with a U.S. beneficial owner that shows little real business activity is a common pattern investigators look for first.

Strict FinCEN Reporting Requirements Facing Modern Taxpayers

Two filings are at the core of FinCEN reporting requirements for individuals: the FBAR and, for certain entities, beneficial ownership information.

FinCEN Form 114 (FBAR): Aggregation Traps and Multi-Account Tracking

FinCEN Form 114, commonly called the FBAR, is required when a U.S. person’s combined foreign account balances exceed $10,000 at any point in the year. This is an aggregate test. Five accounts holding $2,500 each still trigger the FBAR filing requirements, even though no single account crosses the threshold alone.

The table below shows that the gap between non-willful and willful treatment is enormous, which is exactly why late FBAR filing through the correct IRS channel matters more than people expect.

| Violation Type | Maximum Penalty (2026) | Basis |

| Non-willful | $16,536 per report | Per FBAR form filed, not per account (Bittner v. United States, 2023) |

| Willful | Greater of $165,353 or 50% of the account balance | Per account, per year |

| Criminal | Up to a $250,000 fine and 5 years in prison | Up to $500,000 and 10 years if tied to over $100,000 in illegal activity |

The Corporate Transparency Act and FinCEN Beneficial Ownership Compliance

As of March 2025, U.S.-formed companies and their owners are exempt from Corporate Transparency Act beneficial ownership reporting. FinCEN narrowed the rule so that only foreign-formed entities registered to do business in a U.S. state must still file, and even if they do not need to report any U.S. beneficial owners.

This exemption is not permanent. The Eleventh Circuit upheld the law’s constitutionality in December 2025, and FinCEN is expected to issue a final rule sometime in 2026 under current FinCEN regulations. Businesses that assume the obligation is gone for good may face a tight deadline if reporting is reinstated.

Enforcement Escalation: What Triggers an Algorithmic FinCEN Flag?

Modern enforcement relies on pattern detection, not manual review of every filing. A handful of specific behaviors consistently move an account from routine monitoring to active investigation.

Anomalous Cash Movements, Structural Structuring, and Foreign Mismatches

Structuring is the practice of breaking up cash transactions to stay under the $10,000 reporting threshold on purpose. Under 31 U.S.C. § 5324, this alone is a federal felony, punishable by up to 5 years in prison, even if the underlying money was earned legally. A pattern involving more than $100,000 in 12 months raises that maximum to 10 years.

A mismatch between foreign income reported on a tax return and account activity reported through FATCA is one of the patterns that most reliably triggers IRS foreign income audits. Algorithms flag the gap automatically, long before a human examiner reviews the file.

When Regulatory Advisories Transform Individual Accounts Into Targets

FinCEN periodically issues advisories naming specific risk patterns, such as a surge in fraud tied to a particular scheme or region. Once an advisory names a pattern, banks must apply extra scrutiny to any account matching it, which often means IRS agents expand audits to cover related accounts the taxpayer controls.

Proactive Legal Defense Against Financial Surveillance Systems

Once an account is flagged, the choices a taxpayer makes in the first few weeks matter more than almost anything that follows.

Why Advanced Legal Privilege Shielding Beats Standard Compliance Portals

Communications with an attorney are protected by the attorney-client privilege, while conversations with an accountant or a compliance portal generally are not. This distinction matters most once a civil inquiry could turn criminal, because privileged communications cannot be subpoenaed the way unprotected records can.

I have found that taxpayers who consult Verni Tax Law before responding to a soft notice avoid many of the structuring inferences that turn a routine review into a referral.

Anthony N. Verni brings 25 years of experience as an Attorney, CPA, and MBA, and he personally reviews every case rather than handing it to a junior associate. For taxpayers weighing their FBAR defense options, that combination of legal privilege and direct attorney involvement is the protection a portal cannot replicate.

Utilizing Voluntary Disclosure to Correct Historic Reporting Anomalies

Voluntary disclosure means coming forward to fix a filing problem before the IRS finds it first. Taxpayers who qualify for the IRS Streamlined Filing Compliance Procedures can often reduce or eliminate FBAR penalties entirely, since the program is built for non-willful mistakes.

Taxpayers facing willful conduct face a harder path. The IRS Criminal Investigation Voluntary Disclosure Practice closed public comment on proposed reforms on March 22, 2026, which would replace the current 75% civil fraud penalty with a 20% accuracy-related penalty per year.

Until that rule is final, FBAR cases selected for criminal investigation still face the existing framework. A qualified Offshore Voluntary Disclosure Program attorney can help determine which path applies and how to avoid FATCA penalties legally before an examiner opens a file.

Maintaining Compliance in a High-Surveillance Tax Landscape

Financial surveillance in tax enforcement is the current operating model, built on financial crime enforcement network data, automatic FATCA matching, and FinCEN regulations that connect every account a taxpayer touches. The taxpayers who fare best are the ones who treat tax compliance reporting as an ongoing obligation.

Anthony N. Verni knows how IRS systems flag accounts and what it takes to resolve a case before it escalates. He reviews your filing history, identifies gaps before the IRS does, and builds a defense rooted in AML tax compliance knowledge most general practice firms do not have. If financial surveillance has already reached your account, contact Verni Tax Law today for a confidential case review.

FAQs

How exactly does FinCEN data sharing assist the IRS during a targeted tax audit?

FinCEN shares Bank Secrecy Act filings, including SARs, directly with IRS Criminal Investigation, which searched that data in 94% of FY25 cases to match suspicious account activity to specific taxpayers within weeks.

What are the primary global triggers specified under current FinCEN regulations?

The main triggers are structuring cash deposits under $10,000, FATCA mismatches between reported foreign income and account data, and named patterns in FinCEN advisories that prompt IRS agents to expand audits to related accounts.

Who must meet the core criteria for FinCEN reporting requirements annually?

Any U.S. person with foreign account balances exceeding $10,000 at any point in the year must file an FBAR, and foreign-formed reporting companies must file beneficial ownership information under the current Corporate Transparency Act rule.

How does the financial crime enforcement network track domestic shell corporate entities?

FinCEN cross-references bank account openings, TIN verification records, and (for foreign-formed entities) beneficial ownership filings to flag companies with thin business activity relative to their transaction volume.

Can an enterprise entity automate tax compliance reporting to mitigate audit risks?

Yes. Automated TIN matching and transaction monitoring software can catch mismatches before filing, but software alone cannot replace attorney review for entities facing FBAR cases selected for criminal investigation.

What is the structural penalty threshold for an AML tax compliance reporting failure?

Structuring transactions to evade a $10,000 reporting threshold carries up to 5 years in prison under 31 U.S.C. § 5324, rising to 10 years if tied to more than $100,000 in illegal activity within 12 months.