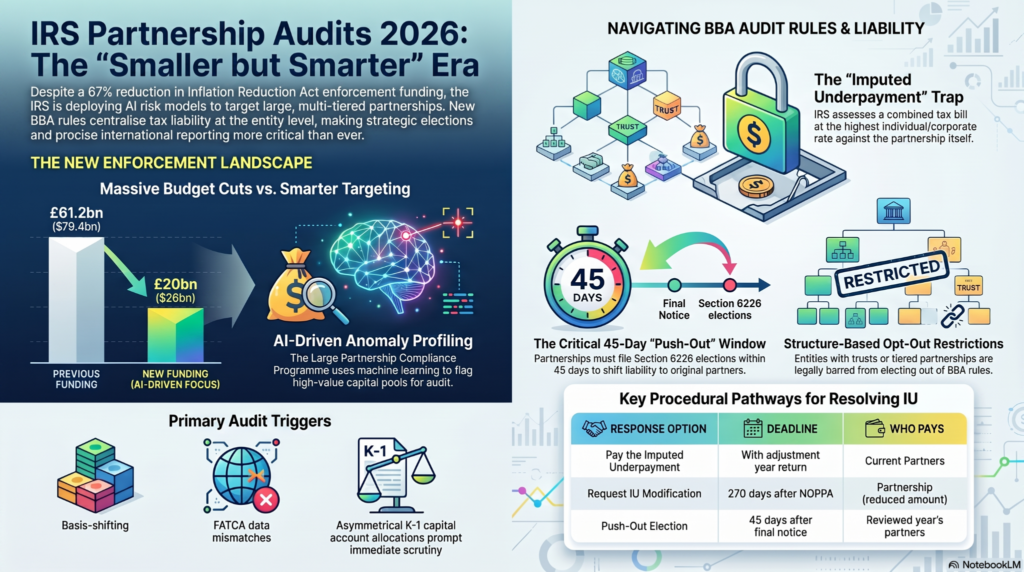

High-net-worth taxpayers tied to partnerships should expect a smaller but smarter IRS partnership audit machine in 2026. Congress cut Inflation Reduction Act enforcement funding from $79.4 billion to roughly $26 billion by February 2026, yet the IRS leans harder on AI to pick targets with that smaller budget.

| Key TakeawaysIRS partnership enforcement funding fell from $79.4 billion to about $26 billion as of February 2026, a cut of $41.8 billionExamination rates on partnerships holding $10 million or more in assets dropped from 2.7% in 2011 to under 0.1% in 2023LB&I now uses AI risk models to select partnership audit targets, though TIGTA called the results “preliminary”A push-out election under Section 6226 must be filed within 45 days of a final partnership adjustment notice2026 FBAR willful penalties can reach the greater of $165,353 or 50% of the account balanceOnly partnerships with 100 or fewer partners, none of them trusts, partnerships, or disregarded entities, can elect out of BBA partnership audit rules |

The 2026 High-Net-Worth Enforcement Initiative: Target Pass-Throughs

The IRS is concentrating its shrinking budget on the largest pass-through entities instead of spreading coverage across every filer. Partnerships holding $10 million or more in assets grew from 140,577 returns in 2011 to 334,686 returns in 2023, while audit coverage shrank, a mismatch that puts high-net-worth structures under sharper scrutiny.

How Federal Funding Shifts Asset Scrutiny to Tiered Entity Structures

Congress reduced IRA enforcement funding from $79.4 billion to about $26 billion by February 2026. The Pass-Through Entities Practice Area lost 20% of its workforce, dropping from 1,079 employees. With fewer agents, the IRS points remaining staff toward multi-tiered partnerships, hedge funds, and real estate vehicles, where one partnership tax audit recovers the most tax per case.

Artificial Intelligence and Anomaly Profiling in Multi-Million Dollar Capital Pools

The IRS uses machine learning inside its Large Partnership Compliance Program to flag IRS partnership audit candidates. TIGTA reported in March 2026 that this AI-driven selection process is still in the early stages. Of 82 of the largest U.S. partnerships reviewed, 92% of closed cases ended with no change to the return, a sign the models are being refined.

Understanding the BBA Partnership Audit Rules Matrix

The BBA partnership audit rules are the centralized system Congress created under the Bipartisan Budget Act of 2015 for partnership returns filed after 2017. Instead of auditing each partner separately, the IRS assesses one combined tax bill, called an imputed underpayment, against the partnership itself. Internal Revenue Code Sections 6221 through 6241 govern nearly every step.

The Entity-Level Trap: How the Imputed Underpayment Mechanism Controls Liability

An imputed underpayment is the tax the IRS calculates at the partnership level after netting adjustments under Section 6225, applying the single highest individual or corporate rate. This usually produces a larger bill than partners would have owed if filing separately. Current partners, not the ones who earned the income, often pay unless the partnership acts fast under the BBA partnership audit rules.

Reviewed Year vs. Adjustment Year: Navigating Complex Ownership Shifts

The reviewed year is the tax year under examination. The adjustment year is the year the audit closes, sometimes years later, when the bill becomes due. A partner who joined after the reviewed year can still absorb the cost unless the partnership pushed liability out to the original partners, creating real exposure for buyers and sellers of partnership interests.

The “Election Out” Myth: Ineligible Partners and Structural Exclusions

Many high-net-worth partnerships assume they can opt out of an IRS partnership audit. Section 6221(b) only permits this for partnerships with 100 or fewer partners, where every partner is an individual, C corporation, S corporation, or estate. One trust, disregarded entity, or tiered partnership anywhere in the chain disqualifies the whole structure, which describes most complex, high-net-worth partnerships.

Operational Stress Testing: Critical Partnership Audit Procedures

Once an audit starts, the partnership representative has four paths for resolving the imputed underpayment, each with its own deadline and consequences for current versus former partners. The table below breaks down what each partnership audit procedure option requires and who pays.

| Response Option | Legal Basis | Deadline | Who Pays |

| Pay the imputed underpayment | IRC § 6225 | With the adjustment year return | Current partners |

| Request IU modification | IRC § 6225(c) | 270 days after NOPPA | Partnership, reduced amount |

| Push-out election | IRC § 6226 | 45 days after the final adjustment notice | Reviewed the year’s partners |

| File an AAR | IRC § 6227 | Before a NOPPA is issued | Depends on the election made |

The Unilateral Authority of the Partnership Representative Designation

The partnership representative holds sole legal authority to bind every partner under Section 6223, and no operating agreement clause can limit that power. Treasury regulations under Section 301.6223-2 void any state law or contract provision that tries to restrict the representative. High-net-worth partnerships should vet this person as carefully as outside counsel, since one signature decides the group’s fate.

Executing the 45-Day “Push-Out” Election Under Section 6226 Mechanics

A push-out election under Section 6226 must be filed within 45 days of the date the IRS mails its final partnership adjustment notice, and the clock does not pause for internal deliberation.

Managing the Administrative Adjustment Request (AAR) Safe Harbors

An administrative adjustment request lets a partnership correct its own prior return instead of waiting for an IRS-initiated partnership tax audit. A BBA partnership cannot file an amended return like a corporation. The AAR must be filed before the IRS issues a notice of proposed adjustment, and the partnership can pay the liability itself or push it out to reviewed-year partners.

High-Risk Triggers Prompting an Immediate Partnership Tax Audit

Certain reporting patterns move a return to the top of the IRS’s selection queue almost automatically. These IRS audit triggers combine balance sheet flags with international gaps, and most are fixable before an examiner opens the file.

Discrepancies in Foreign Asset Declarations, Cross-Border Allocations, and FATCA Links

FATCA data-sharing risks rise sharply when a partner’s Form 8938 figures do not match what a foreign bank reported under intergovernmental agreements. These FATCA-related IRS audits usually start from a mismatch.

FBAR compliance requirements trigger once foreign accounts exceed $10,000 during the year, while Form 8938 thresholds start near $50,000. Gaps in foreign account reporting compliance lead to cross-border IRS enforcement actions against the partnership and its partners.

Asymmetrical K-1 Capital Account Disclosures and Non-Economic Loss Allocations

Basis-shifting transactions, where related partners move tax basis between entities taxed at different rates with no real economic change, sit near the top of LB&I’s campaign list. K-1 capital accounts that swing without a matching cash or property event are among the clearest factors that increase IRS audit risk. These patterns also explain why IRS agents expand audits from one open year into several once an anomaly surfaces.

Advanced Defense Frameworks for High-Value Corporate Entities

Standard bookkeeping cannot protect a partnership once an exam edges toward fraud allegations. Strong IRS audit defense strategies separate routine accounting from privileged communication before any notice arrives.

Why Standard Accounting Protocols Fail to Preserve Critical Legal Protections

Tax return preparation and routine bookkeeping are never privileged, regardless of confidentiality promises. Once the partnership’s regular accountant starts analyzing audit risk, courts often treat that work as business advice, not legal strategy. Bringing in counsel after the IRS has the file is usually too late.

Leveraging Attorney-Client Privilege During Comprehensive Document Production

A Kovel arrangement, named for the 1961 federal case that created it, lets an attorney hire an accountant to work under the attorney’s privilege instead of the accountant’s own engagement. This keeps forensic analysis and defense strategy out of the IRS’s hands during document production.

Anthony N. Verni of Verni Tax Law structures these protections from the first call, pairing attorney and CPA standing so legal and accounting analysis come from one desk instead of two.

Securing Wealth Defenses Against Algorithmic IRS Campaigns

IRS enforcement in 2026 runs on less money but sharper targeting. High-net-worth partnerships face an agency using AI to find the highest-value partnership tax audit candidates instead of casting a wide net, so complex, multi-tiered structures carry more exposure even as overall audit rates keep falling.

Verni Tax Law brings 25 years of combined legal and accounting experience to exactly this exposure. Anthony N. Verni personally handles every case as both attorney and CPA, covering FATCA compliance, FBAR penalty defense, civil tax litigation, and responding to IRS tax fraud allegations for partnerships, trusts, and partners with cross-border holdings, offering experienced IRS audit representation instead of a one-size-fits-all template.

He reviews your ownership structure, push-out elections, and foreign filings before the IRS asks a question, then builds a defense around what your facts support. Contact us today for a confidential case review.

FAQs

What initiates a high-priority partnership audit for global high-net-worth investors?

Balance sheet discrepancies over $10 million, mismatched FATCA data, and basis-shifting between related partners are the three fastest triggers for a high-priority partnership audit.

How does the IRS structure an entity-level IRS partnership audit for complex structures?

The IRS computes one imputed underpayment at the partnership level, taxed at the highest individual or corporate rate, instead of auditing each partner’s return separately.

What specific transactional patterns quickly spark a targeted partnership tax audit?

Asymmetrical K-1 capital account allocations, basis shifts between related partners facing different tax rates, and non-economic loss allocations are the patterns examiners flag fastest.

Who is restricted from exercising an annual opt-out under BBA partnership audit rules?

Partnerships with a trust, another partnership, or a disregarded entity as a partner cannot elect out, no matter how few total partners the partnership has.

What timeline restrictions govern standard federal partnership audit procedures?

Partnerships get 45 days after a final adjustment notice to push out liability under Section 6226, and 270 days to request imputed underpayment modification.

How can international investment funds safeguard long-term partnership tax compliance?

Filing accurate FBARs and Forms 8938, auditing K-1 allocations annually, and naming a partnership representative bound by a written operating agreement cut audit risk the most.