If your foreign accounts, crypto wallets, or offshore assets need reporting, FATCA compliance is the system that keeps U.S. taxpayers visible to the IRS. Swiss banking secrecy ended in 2009, and a global international tax reporting machine now reaches nearly every foreign account and foreign crypto wallet under the Foreign Account Tax Compliance Act.

In this blog, we will explain what FATCA compliance means, what you must report, and how to avoid costly mistakes while staying fully compliant.

| Key TakeawaysUBS paid $780 million and disclosed thousands of client names in 2009, ending Swiss banking secrecyFATCA filing requirements start at $50,000 for single filers living in the U.S.FBAR threshold stays at $10,000; willful FBAR penalties reach $165,353 or 50% of the account balanceFATCA vs. CRS: the U.S. participates in FATCA but not the 120-country CRS networkForm 1099-DA started tracking crypto broker transactions on January 1, 2025Modern FATCA filing requirements and FATCA reporting requirements now connect directly to offshore account reporting, foreign financial asset reporting, FATCA disclosure rules, and foreign bank account compliance rulesStreamlined Filing Compliance Procedures charge a 5% penalty instead of stacked FBAR fines |

The Fall of Offshore Secrecy: How Swiss Banking Changed Forever

Swiss banking secrecy ended in February 2009, when UBS admitted helping U.S. clients hide assets, paid a $780 million settlement, and disclosed thousands of account holder names. That case built the foreign bank account compliance framework behind today’s offshore account reporting rules and founded modern FATCA disclosure rules.

How Traditional Offshore Accounts Evaded Detection

Traditional offshore accounts evaded detection because no automatic exchange existed between foreign banks and the IRS, so offshore account reporting did not happen at scale.

A U.S. person could open a Swiss account and skip foreign bank account compliance, since secrecy laws made disclosure a crime. Expat tax compliance and U.S. expat tax reporting simply did not exist for offshore holders.

Why the U.S. Needed a Global Compliance Framework

The U.S. needed a global compliance framework because voluntary disclosure alone could not close the gap left behind. More than 14,700 taxpayers came forward after UBS, but that only scratched the surface. Congress answered in 2010 with the Foreign Account Tax Compliance Act, enforcing foreign bank account compliance worldwide and creating the first true international tax reporting system.

What Is the Foreign Account Tax Compliance Act (FATCA)?

The Foreign Account Tax Compliance Act is a 2010 law requiring foreign institutions to report American account holders to the IRS or face steep withholding. FATCA regulations force banks to identify U.S. customers and share data, closing the gap that once shielded UBS-style accounts under outdated FATCA disclosure rules.

The Core Objectives of Modern FATCA Regulations

FATCA regulations exist to stop taxpayers from hiding income abroad. The Foreign Account Tax Compliance Act works two ways: institutions handle FATCA reporting requirements to the IRS, while taxpayers separately disclose under their own FATCA disclosure rules, forming a closed international tax reporting loop.

Banks refusing foreign bank account compliance face a 30% withholding tax on U.S.-source payments. This pushed nearly every major foreign bank into FATCA compliance within years, reshaping FATCA regulations overnight and folding every FATCA filing requirements deadline into routine compliance calendars.

Who Qualifies as a “U.S. Person” Under Global Transparency Regimes?

A “U.S. person” under FATCA disclosure rules includes citizens, green card holders, and certain resident aliens, regardless of where they live. This catches Americans abroad as easily as at home under global international tax reporting norms, which is why U.S. expat tax reporting carries the same FATCA filing requirements as domestic filing.

Dual citizens, accidental Americans, and long-term green card holders overseas all fall under this category. Expat tax compliance depends on citizenship, not residence, under every FATCA disclosure rules framework, and the same logic governs international tax reporting and offshore account reporting broadly.

Navigating Modern FATCA Reporting Requirements

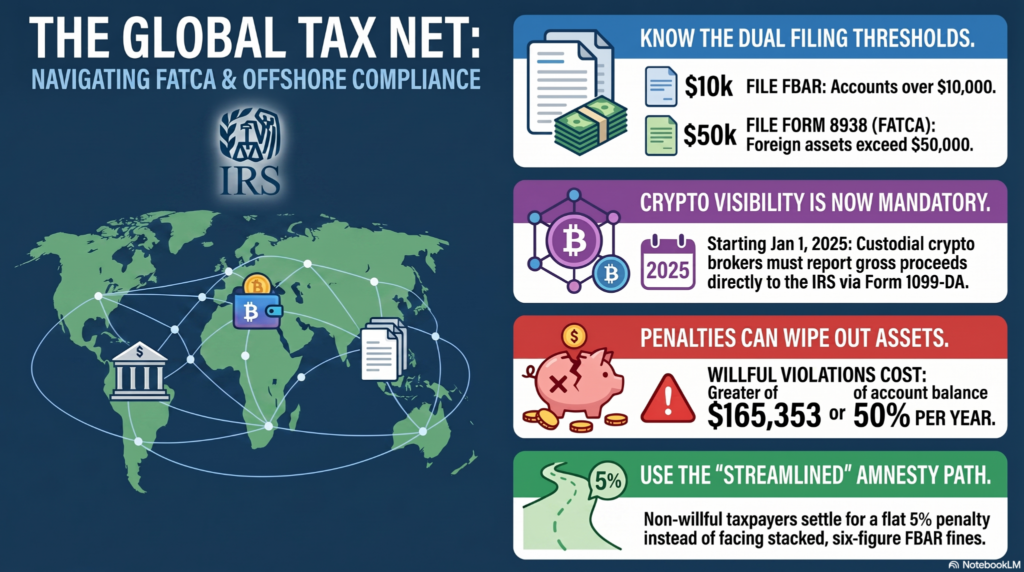

FATCA reporting requirements center on Form 8938, filed with your tax return once foreign assets exceed the set FATCA filing requirements thresholds. Form 8938 filing requirements apply on top of, not instead of, any separate FBAR obligation under broader foreign financial asset reporting and offshore account reporting norms.

IRS Form 8938 vs. FBAR (FinCEN Form 114): What is the Difference?

Form 8938 and FBAR are separate filings with different agencies, thresholds, and scopes. Form 8938 satisfies FATCA reporting requirements with the IRS, starting at $50,000 for single filers. FBAR reports to FinCEN and apply once foreign accounts exceed $10,000 combined.

The table below compares both forms as part of any solid FATCA compliance checklist. Filing one does not satisfy the other; taxpayers handling FBAR and FATCA reporting together often file both in the same year.

| Feature | Form 8938 (FATCA) | FBAR (FinCEN Form 114) |

| Filed with | IRS, attached to Form 1040 | FinCEN, separate from tax return |

| Threshold (single, U.S. resident) | $50,000 year-end / $75,000 any time | $10,000 aggregate, any time |

| Covers | Securities, foreign entity interests, pensions | Foreign bank and financial accounts only |

| Non-filing penalty | $10,000, up to $50,000 for continued failure | Up to $16,536 per violation (non-willful) |

This shows why FBAR and FATCA reporting rarely substitute for each other, and why every FATCA compliance checklist tracks both forms separately, alongside any FATCA data sharing the IRS already receives.

FATCA Filing Thresholds for Domestic and Overseas U.S. Taxpayers

FATCA filing requirements scale by residency under documented foreign bank account compliance guidance. Single U.S. residents meet Form 8938 filing requirements once foreign assets exceed $50,000 year-end or $75,000 any time; joint filers face $100,000 year-end or $150,000 any time.

Taxpayers abroad get higher FATCA filing requirements thresholds under the same foreign financial asset reporting rules, such as $200,000/$300,000 single, $400,000/$600,000 joint. In our practice, expat clients confuse these tiers constantly, assuming domestic FATCA reporting requirements apply under standard foreign bank account compliance.

Which Specified U.S. Taxpayer Foreign Assets Must Be Reported?

Specified foreign financial assets include foreign bank accounts, foreign stocks, foreign partnership interests, and foreign mutual funds. Foreign financial asset reporting casts a wider net than FBAR, capturing investments that never touch a bank account, plus foreign pensions, life insurance, and trust interests. This trips up clients who assume retirement accounts abroad fall outside the offshore account reporting scope under FATCA disclosure rules; they almost never do.

The New Frontier: Blockchain, Crypto, and Digital Asset Enforcement

Digital assets created a reporting gap that the Foreign Account Tax Compliance Act never anticipated in 2010. The IRS closed part of that gap through a separate domestic law, while global foreign financial asset reporting frameworks raced to catch up with crypto holdings.

Does FATCA Apply to Foreign Crypto Exchanges and DeFi Wallets?

FATCA may apply to foreign crypto exchanges if the exchange qualifies as a Foreign Financial Institution holding an account for a U.S. person, though the IRS has not issued explicit guidance under current FATCA regulations or broader international tax reporting rules. Exchanges offering custody or trading services to American users increasingly register to satisfy foreign bank account compliance and avoid the 30% withholding penalty.

Noncustodial DeFi wallets sit in a different category, since the user holds the private keys directly and no institution intermediates custody under the Foreign Account Tax Compliance Act’s “financial account” definition. This remains an evolving area, and FATCA enforcement risks for crypto holders depend heavily on platform structure, making FATCA enforcement risks a moving target for any digital asset holder abroad.

From Form 8938 to Form 1099-DA: The Rise of Digital Asset Proceeds Tracking

Form 1099-DA is the IRS return that custodial digital asset brokers must file to report gross proceeds from crypto sales, starting with transactions on or after January 1, 2025. This domestic broker rule works alongside, not as a replacement for, FATCA compliance and FBAR obligations under broader FATCA regulations.

FBAR reporting for cryptocurrency remains legally unsettled. The IRS has not confirmed that crypto accounts trigger FBAR, though crypto on a foreign exchange that also allows fiat deposits often falls under foreign financial asset reporting regardless. We typically recommend clients handle FBAR reporting for cryptocurrency conservatively rather than gamble on regulatory silence.

Severe Consequences of Failing to Maintain FATCA Compliance

FATCA non-compliance penalties start at $10,000 for a missed Form 8938 filing and escalate fast under current FATCA regulations. Exposure grows larger once FBAR and accuracy-related penalties stack on the base failure.

Civil Monetary Penalties and Costly Internal Revenue Service Audits

A failure to file Form 8938 carries a base $10,000 penalty, climbing to $50,000 if it continues after IRS notice. IRS audits for foreign income frequently uncover gaps in foreign financial asset reporting, and once flagged, the audit often expands into full FBAR review.

Non-willful FBAR violations carry penalties up to $16,536 per violation under 2025 inflation adjustments, though the IRS frequently waives these for reasonable cause if no prior IRS audits for foreign income exist. Form 8938 filing mistakes, such as undervaluing an account, can trigger a 40% accuracy-related penalty on related tax underpayment, and these FATCA non-compliance penalties compound fast across multiple years.

Willful Non-Compliance and Criminal Prosecution Risks

Willful FBAR penalties reach the greater of $165,353 or 50% of the account balance per violation, adjusted annually for inflation. This applies per year, so a multi-year willful violation can exceed the account’s total value, and willful FBAR penalties of this size rarely come alone.

Criminal exposure adds another layer: fines up to $500,000 and prison terms up to 10 years under federal law. After the UBS settlement, the Justice Department secured guilty pleas from multiple American account holders, with sentences including six-figure fines and incarceration. Avoiding FATCA penalties of this severity requires acting before the IRS makes first contact.

Proactive Remediation: Streamlined Compliance Procedures & Legal Protections

Offshore voluntary disclosure options exist for taxpayers who discover unfiled FBARs or Form 8938s before the IRS contacts them first, and choosing the right offshore voluntary disclosure option track determines the entire penalty outcome. The Streamlined Filing Compliance Procedures charge a flat 5% penalty on the highest aggregate balance over six years, replacing stacked FATCA non-compliance penalties that could otherwise reach six figures.

To qualify, a taxpayer must certify that the prior non-compliance was non-willful under FATCA disclosure rules and foreign bank account compliance standards, meaning a genuine misunderstanding rather than intentional concealment. Taxpayers amend the three most recent tax years and file FBARs for six years.

Willful violations require the IRS Criminal Investigation Voluntary Disclosure Practice instead. Offshore tax compliance assistance at this stage means building a foreign account penalty defense around an honest, willful versus non-willful assessment, since the wrong certification creates new exposure.

Protecting Your Global Wealth in a Fully Transparent Era

Swiss banking secrecy ended permanently in 2009, replaced by a worldwide international tax reporting network covering bank accounts, securities, and digital assets under unified FATCA reporting requirements. FATCA compliance is the baseline expectation for any American holding assets outside the United States. Penalties for getting it wrong, from $10,000 Form 8938 failures to six-figure willful FBAR penalties, make proactive correction far cheaper than discovery.

Verni Tax Law built its practice around this transparency era of international tax reporting. Anthony N. Verni is a Tax Attorney, CPA, and MBA with 25+ years of IRS experience handling FATCA compliance, FBAR, and offshore account reporting disclosure for clients across New Jersey, New York City, and South Florida.

He helps you determine whether your non-compliance qualifies for Streamlined Filing Compliance Procedures, correct Form 8938 filing mistakes before an audit, and build a foreign account penalty defense if the IRS has already made contact. Contact Verni Tax Law today for a confidential review of your offshore reporting position.

FAQs

What is the main difference between an FBAR and FATCA compliance filings?

FBAR reports to FinCEN at a $10,000 threshold; FATCA compliance through Form 8938 reports to the IRS starting at $50,000 for single U.S. residents.

What specific information is covered under the Foreign Account Tax Compliance Act?

The Foreign Account Tax Compliance Act covers foreign bank accounts, foreign securities, foreign partnership interests, foreign pensions, and foreign-issued insurance with cash value.

Who is required to meet annual Form 8938 FATCA reporting requirements?

U.S. citizens, green card holders, and certain resident aliens exceeding their applicable threshold must meet FATCA reporting requirements annually under standard FATCA filing requirements.

Does offshore account reporting apply to real estate or only liquid financial accounts?

Directly held foreign real estate is excluded from offshore account reporting, but real estate held through a foreign entity often triggers foreign financial asset reporting on that entity’s interest.

How does the IRS locate undisclosed US taxpayer foreign assets held abroad?

The IRS uses FATCA data sharing from over 110 countries’ institutions, cross-referencing bank data against individual international tax reporting filings automatically.

What are the current asset thresholds specified under FATCA regulations?

Single U.S. residents report at $50,000 year-end or $75,000 any time; FATCA regulations set higher thresholds of $200,000 and $300,000 abroad, with FATCA vs. CRS rules differing sharply outside the U.S.